What is a Recession?

What is a Recession?

How to understand GDP growth and everything else

Background

I don’t think I’ve mentioned it on this blog before, but I have a master’s degree in economics. Despite this, I’ve mostly avoided economics articles, mostly because I don’t have much confidence in my viewpoints. I see tradeoffs and uncertainty where others see consistent confirmation of their worldviews. I could probably write some more “man, I dunno” type posts (like this one), but I don’t know who would find them enlightening.

On top of that, I dislike credentialism and the insistence on “trusting the experts.” Many of us have worked with unimpressive individuals who insisted upon their MBA or Lean Six Sigma certification. In my experience, I find people high general intelligence and conscientiousness more productive than anyone with an alphabet soup appended to their name on LinkedIn. I’m not claiming that expertise doesn’t exist, but I don’t think we can quantify it through degrees, job titles, and online certifications. Without any formal credentials, I’ve gained enough hands-on experience with machine learning to write multiple posts about the topic.

Hence, I’m not going to expect anyone to accept my conclusions due to some diploma that collects dust in the closet. I’m only going to ask my readers to accept that I have more familiarity with economic data than the average person. As a graduate student, I created recurring reports covering national and regional economic data. Did you know that the unemployment rate comes from a survey of households, while the jobs number comes from a survey of establishments? Did you know that the BLS seasonally adjusts these figures to account for the Q4 hiring boom? Do you check the retail sales report around 15th of every month? If not, that’s fine! You shouldn’t parrot those who do. You should just remain open the fact that you could learn from those who do.

In the past week, you’ve probably read analysis like this, from the Common Sense Substack:

→ It’s not a recession if Biden didn’t see his shadow: With news that the economy shrank by 0.9% in the last quarter, you might think that we’ve entered a recession, which is commonly defined as an economy shrinking for two consecutive quarters. But that old way of thinking is over. Recession is a very mean word that we don’t use under President Biden. The White House is denying all past statements from White House officials who used the old forbidden definition: “That’s not the definition,” the press secretary said this week when confronted with the banned one.

[…]

The media is ready to go carrying the administration’s water. Here’s the Associated Press: “By one common definition—the economy shrinking for consecutive quarters—the U.S. economy is on the cusp of a recession. Yet that definition isn't the one that counts.” Online encyclopedias and social media are following suit. The Wikipedia page on “recession” is getting furiously updated.

Subtask readers seem to love this sort of writing, and I can understand why. I also don’t like how mainstream outlets cover these sorts of issues. In fact, you probably wouldn’t be reading this blog if you held the mainstream media in high regard. Skepticism of authority is a positive instinct. An instinct, however, isn’t an argument. As I’ve written about previously, it doesn’t really matter if a proposition undermines the authorities. We should hold beliefs that correspond to facts. Sometimes, the facts own the elites. Other times, they don’t. If you want to find the truth, you’re going to need to focus on evidence and reason, not edginess.

Of course, I’ll acknowledge that there’s tons of political expediency occurring here. If Trump were an office, I’m sure Democrats would insist on the two-quarter-drop (TQD) definition of a recession while Republicans would highlight the National Bureau of Economic Research (NBER) one. Yup, politicians act cynically. I get it. It’s also pathetic to see Wikipedia, the AP, and other resources change their definitions for political expediency. It’s hard to imagine these institutions doing the same for Trump.

To paraphrase my earlier article, though, pathetic things can be true. Since I started working with macroeconomics data, I never understood a recession to mean two quarter of negative GDP growth. I always thought of recessions as the gray bars on FRED1 graphs. Macroeconomics professors would remind us to use that data, rather than a TQD, as the definition of a recession. I remember a professor citing the TQD as an indicator that someone has never analyzed macroeconomic data. The NBER didn’t change it either. You can read the NBER page from back in late 2020, which says

The NBER's definition emphasizes that a recession involves a significant decline in economic activity that is spread across the economy and lasts more than a few months.

[…] Because the BEA figures for real GDP and real GDI are only available quarterly, the committee considers a variety of monthly indicators to determine the months of peaks and troughs. It places particular emphasis on two monthly measures of activity across the entire economy: (1) personal income less transfer payments, in real terms, which is a monthly measure that includes much of the income included in real GDI; and (2) payroll employment from the BLS. Although these indicators are the most important measures considered by the committee in developing its monthly business cycle chronology, it does not hesitate to consider other indicators, such as real personal consumption expenditures, industrial production, initial claims for unemployment insurance, wholesale-retail sales adjusted for price changes, and household employment, as it deems valuable.

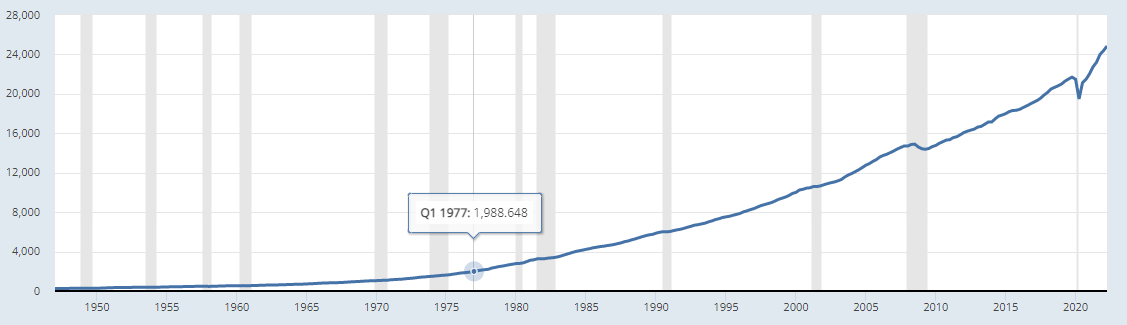

In other words, a recession occurs when a bunch of indicators head in the wrong direction. A TQD usually coincides with a recession, but it’s neither necessary nor sufficient. You will probably recognize this definition of a recession if you’ve seen a graphs like this:

What Doth GDP Growth?

Let’s start with the basics. The Common Sense article claims that “the economy shrank by 0.9% in the last quarter.” A reader might interpret that as a Q2 2022’s real2 GDP being 0.9% lower than Q1’s. In my personal life, I’d call that “close enough,” but, on this blog, it might worth delving into the details.

To start, Q2 contains fewer days than Q1. I’ve advocated for the Earth to hasten its rotation to 364 days, allowing for 13 months of 28 days each. It has ignored me (jerk), so we’re stuck with uneven quarters. There’s also a general economic decline in Q1 following the Christmas splurge of Q4. The GDP figures correct for this, so we’re comparing “seasonally adjusted” figures rather than raw numbers. Economists also annualize these numbers, so the figures look more like a one-year total3. Finally, you probably assume that the Q2 2022 numbers include, you know, the second quarter of 2022. You’d be wrong! You won’t see that for at least another month. Until then,

The advance estimate of GDP for the second quarter is based on source data that are incomplete and subject to updates. Three months of source data were available for consumer spending on goods; shipments of capital equipment; motor vehicle sales and inventories; manufacturing, wholesale, and retail trade inventories; exports and imports of goods; federal government outlays; and consumer, producer, and international prices. For major source data series for which only two months of data were available, or for which data for the second quarter are not yet available, BEA's assumptions were based on a variety of sources, most notably: private high-frequency payment card transactions data, industry and trade association reports that include volume data, such as health care patient visits and traveler throughput, as well as recreation services revenues and event attendance

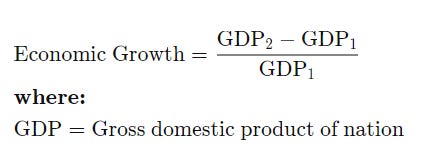

All right, so once we account for seasonality and missing data imputation, we can rest assured that the Q2 GDP figure was 0.9% lower than the Q1 number, right? Let me check the top three Google results for how to calculate GDP growth.

To calculate the growth rate for both nominal and real GDP, two data years are needed. The GDP of year 2 is divided by the GDP of year 1 and the answer is subtracted by one. That is, Growth Rate = (GDP_Year2/ GDP_Year 1) - 1.

GDP growth = (GDP in current period - GDP in the previous period) / GDP in the previous period * 100

3. Investopedia provides a helpful format:

Sounds easy. I’ll head to the BEA (Bureau Of Economic Analysis) website and retrieve the Q2 and Q1 annualized, real, seasonally adjusted GDP figures. We have 19,681.7 in Q1 and 19,727.9 in Q24. Just plug it into the formulas shown above and we calculate… a -0.2% dip in GDP? Huh?

What happened here? Simply put, the first three Google don’t work for the annualized GDP figures, and both the media and government organizations almost never present non-annualized GDP figures. Basically, they’re wrong. Here’s the correct calculation from the BEA:

Plug the numbers into that, and you’ll obtain the expected -0.9%.

That’s based on Real GDP, by the way, which adjusts for inflation. Calculating inflation is no easy task, but I’ll leave that topic for another day.

The Point

You don’t need to understand all the nuances of GDP growth calculations to hold an informed opinion on the topic. Still, I hope I’ve shown that there’s more fuzziness to that figure than you presumed. Given that, maybe you can understand the problem with defining recessions via small GDP fluctuations. After you consider seasonal adjustment, data imputations, annualization, and inflation, a 0.9% dip might not indicate anything signficant.

Even if GDP figures didn’t feature these caveats, there’s other reason to reject the TQD definition of a recession. I could note that 1947 saw a TQD without a recession, but I doubt anyone cares about an event from 75 years ago. Instead, I’ll run through an example that merely feels like 75 years ago: early 2020.

Due to the coronavirus and it’s corresponding shutdowns, the quarterly GDP5 looked like this:

The gray bar represents the Coronavirus Recession, which only lasts one quarter: Q2 2020. Yes, GDP also fell in Q1 2020, but the NBER would have declared a a recession without that decline. That probably sounds confusing, so let me run through a thought experiment.

The Coronavirus lockdowns started, as best I can recall, in mid-March of 2020. That’s the driver of the small dip before the recession in the Q1. Imagine that growth from January 1st to mid-March was so strong that it overpowered the economic devastation from two weeks of closures. Alternatively, imagine that virus took a bit longer to make it to the United States, and shutdowns started on April 1st. If you want to get really funky, imagine that the Julian calendar started at a different day such that we call mid-March in our timeline was actually early April in another one.

In all these cases, we would see the same economic downturn: falling GDP, rising unemployment, and cratering retail sales, but it would all occur in a single quarter. We’d get the Coronavirus Recession without a TQD. Now, imagine this occurred while someone you hate sat in Oval Office: Donald Trump, Joe Biden, Tom Brady. This president looked the American people in the eye and told us there was no recession since GDP didn’t fall in two consecutive quarters. Would you agree with him? Or would you think it was cynical wordplay? If you chose the latter, then you agree that we can’t define a recession as TQD.

We could picture other scenarios where TQD definition doesn’t work. Imagine an economy saw -10% growth in Q1, +0.1% growth in Q2, and -10% growth in Q3, alongside a corresponding rise in unemployment and decline in personal income. Would you also consider that a non-recession? On the other hand, imagine an economy with +10% growth in Q1, -0.1% in Q2, -0.1% in Q3, and 10% in Q4, this time with rock-bottom unemployment and consistent wage growth throughout the whole year. That doesn’t seem like a recession. In other words, I don’t think the TQD definition captures either the academic or intuitive meaning of the term “recession.” The AP might have changed their definition for cynical reasons, but they changed it from the wrong one to the right one.

The Real Point

So, are we currently in a recession? I’d say no, as I can’t really square a recession with one of the lowest unemployment rates on record. I could see counterarguments to that, of course, such as the number of young men outside the labor force. Regardless, the best answer is that it probably doesn’t matter. People focus on the wellbeing of themselves, their peers, and their family. Only weirdos like me care where the BEA adds gray bars to a chart. Most importantly, we need to improve peoples’ lives whether there’s a recession or not.

Ultimately, I didn’t just write this to explain GDP calculations, though I had A LOT of fun doing so. I also want to show the shortcoming of reflexively edgy thinking. That same Common Sense article discusses the recent findings related to SSRIs and depression, summarizing it as

→ Fake science: In one week, three major debunkings are a good reminder that “trust the science” is silly. Science is always a work in progress.

First: Depression seems to have nothing to do with a chemical imbalance. All that talk about how depressed people don’t make enough serotonin? It’s not really true—at least according to a new study.

No such debunking of chemical imbalances occurred, just meta-study questioning a straightforward linkage between depression and dearth of serotonin. However, as psychotherapist Scott Alexander argues, psychiatry has never relied on this simplistic relationship between serotonin and depression:

…anyone who said that depression was caused solely by serotonin deficiency wouldn’t just be failing as a scientist, but also failing as a drug company shill. Pfizer spent billions of dollars on Effexor, which hits norepinephrine as well as serotonin, and they’re just going to dismiss all of that as useless? GlaxoSmithKline has Wellbutrin, which hits dopamine and norepinephrine and maybe acetylcholine but doesn’t get serotonin at all.

Did you know that? I didn’t! That’s the sort of relevant information you’ll learn from someone who’s spent a lot of time understanding the issue. No, you shouldn’t blindly “trust the experts,” but you should also understand that, for many topics, some people know more than you.

At my first post-graduate job, I received positive evaluations for my performance and negative ones for my attitude. Leaders said I was too cynical and dismissive, which hurt my ability to understand the needs of the business and grow as a professional. This advice felt condescending at the time, but I can see its value in retrospect. Though I still see tons of nonsense in the workplace, I can’t deny that these leaders got something right. It’s important to listen to and understand the other side before declaring something bunk or “debunked.” We could all use a bit more curiosity.

St. Louis Federal Reserve, the best resource for macroeconomics data.

“Real” means adjusted for inflation. All figures will be real unless otherwise noted. The opposite of real is “nominal.”

For example, the Q2 number shows Q2 as if it were the year. A quarter may only have $5T of output, but will report $20T as the “annualized.”

Both figures in billions of 2012 USD, annualized.

These are nominal figures, not adjusted for inflation. I thought I’d display both so that you’re familiar with the approximate levels of each.

Thank you for this very helpful article! I particularly like how you connected your economic analysis with the alleged debunking of SSRIs. As you note, neuroscientists never said that depression was caused solely by low serotonin; that was a media misunderstanding (or misrepresentation). It’s useful to listen to people who actually know something about a topic!

One thing about Wikipedia is that anyone can edit it, but those editing it are more committed to their truth. I edit Wikipedia but on non-controversial topics usually. At the top of each page is a "watch" tab that alerts you if a page you watch has been changed. The "team" with the most determined editors usually wins. Also, since one has to cite an article to make a point the side with more published articles gets the final say. I can't, for example, cite this Substack article because Wikipedia won't allow citations to websites (stupid) but the weight of truth lies in academic journals, so it is sort of a loaded process.